Artemis Strategic Bond Fund update

The fund's managers review a quarter in which strong returns from its holdings in investment-grade and high-yield bonds saw the Artemis Strategic Bond Fund generating a positive return – and outperform its peers.

Source for all information: Artemis as at 30 June 2024, unless otherwise stated.

Performance

The fund returned 0.5% over the quarter, just ahead of the average return of 0.4% from its IA peer group. Over the year to date, meanwhile, it has returned 1.9% versus an average return of 1.3% from its peers.

Considering that yields rose significantly over the first half of 2024, pushing government bond prices lower, the fund’s positive return emphasises the attractions of the ‘all in’ yields currently available across much of the fixed-income universe. Those yields offer a useful form of cushioning against any further rise in bond yields.

Over the quarter:

- The fund’s longer duration position relative to its peer group acted as a drag on its relative performance.

- Set against that, our dynamic, tactical shifts in the fund’s duration positioning and in its cross-market exposure had a positive impact.

- The fund’s credit positions performed well – particularly those in short-dated high-yield bonds. We retain a strongly positive view of this part of the bond market.

| Q2 2024 | Year to date | One year | Three years | Five years | Ten years | |

|---|---|---|---|---|---|---|

| Artemis Strategic Bond Fund | 0.5% | 1.9% | 10.3% | -1.5% | 7.3% | 31.5% |

| IA Strategic Bond | 0.4% | 1.3% | 8.9% | -3.5% | 6.0% | 25.4% |

Government bonds (18% of the fund)

We still believe that we are in the later stages of the interest-rate cycle and that we are moving closer to the point at which we see all of the world’s major central banks – rather than just a select few – cutting rates. Accordingly, the fund maintained a duration of around six years over the quarter; this is above the mid-point of its permitted range (three to eight years of duration) as well above its long-term average (five-and-a-half years).

We have increased the duration of the Artemis Strategic Bond Fund up to a 6 ~ 6.5 year range

We further increased the fund’s sensitivity to rate cuts going into the end of the quarter as US economic data continued to deteriorate. In our view, it seems possible that the US Federal Reserve will start cutting rates in the third quarter of this year.

Investment-grade bonds (51% of the fund)

Within the investment-grade market, we shifted some of the fund’s UK property exposure out of Blackstone and into Tesco’s property-secured bonds and bonds secured on Sheffield’s Meadowhall Shopping Centre. We also added bonds issued by UK industrial property operator Prologis.

Elsewhere, we subscribed to a new issue of long-dated bonds by UK energy supplier Centrica, continued to add to the fund’s position in UK pub operator, Mitchells & Butlers and reduced the fund’s exposure to Thames Water.

In financials, we reduced our positions in ING, Admiral Group, Deutsche Bank and Met Life and sold out of Investec’s subordinated bonds. Set against this, we increased the fund’s exposure to Lloyds Bank, Coventry BS and Danske Bank.

High-yield bonds (28% of the fund)

We took a small position in Picard, a French food retailer. Picard sells high-quality frozen food to affluent urban consumers and occupies an attractive niche in French life, where consumers see frozen food as a premium option. The company issued new five-year euro-denominated bonds and, due to French political tumult, they came at what we regarded as a very attractive price.

We also invested in US kitchen and bathroom cabinet maker Masterbrands. This is a horizontally integrated consolidator of what has historically been a fragmented industry. It benefits both from the construction of new homes and from increased renovation activity as people choose to stay in existing properties longer. We established a position in US equipment-rental chain Herc Holdings, which benefits from low leverage and enjoys significant economies of scale.

We trimmed the fund’s holdings in records-management company Iron Mountain, payments provider Worldpay and US concrete-pumping specialist Brundage Bone.

Outlook

Inflationary pressures continue to moderate – and rate cuts are coming

This is the central fact that informs our positive view on the bond market. It seems quite clear that most developed-market central banks (except for maybe those in New Zealand and Norway) would like to cut rates to help ensure a soft landing.

There are risks, however. Some economic indicators suggest that the global economy is doing better than expected. After growing at a ~3.5% rate in the second half of 2023, economic growth in the US is now showing signs of slowing to a more ‘normal’ pace. And there are early signs of weakness coming through in the labour market (Jolts data and initial jobless claims both point to a more pronounced slowdown in hiring). But this is not yet showing up in official payroll releases; we will need to see hard evidence before we can definitively say the US economy is at risk of a significant slowdown.

There are, meanwhile, reasons for optimism about the UK and European economies, which look set to reverse their recent pattern of anaemic underperformance relative to the US. Energy bills are falling and real incomes are rising at a faster pace than at any time since the start of the pandemic, boosting the financial positions of households who are putting the worst of the rate-hiking squeeze behind them. Today, there must be some risk that the Bank of England cuts rates too soon, obliging it to rein in dovish market expectations later this year should economic growth and inflation come in stronger than it expects.

We continue to favour shorter-dated bonds

While we are positive on prospects for bond market, we remain cautious towards longer-dated bonds. We cannot ignore the threats posed by political populism. This is not just a French issue and it presents risks to bond markets in two main ways. One risk is that fiscal deficits widen even further, adding to outsized debt burdens and resulting in an increased supply of government bonds. A second risk is that rising protectionism reawakens inflation.

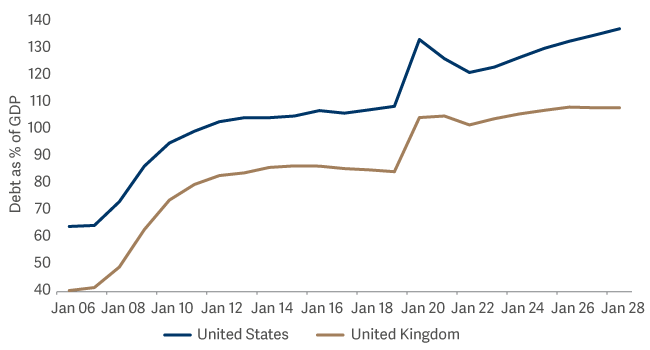

Debt as a % of GDP has surged

This is one reason why we don’t see yields towards the long end of the curve (10-years and more) moving substantially lower over the next 12 months. Towards the shorter end of the curve, however, we continue to believe that the actions of central banks (rate cuts) will outweigh forces pulling in the other direction (political populism and rising bond supplies). There is a possibility that central banks will have to cut rates by more than the market is currently pricing – and the potential gains under that scenario are sufficient to compensate us for the risks posed by the fractious political environment.