Taylor Swift, Harry Kane or Keir Starmer: Who will be most important for UK investors this summer?

The general election may be dominating headlines in the financial pages, but Ed Legget says it is likely to have little impact on the UK market in the long term – while in the short term, economic stimulus is likely to come from other sources.

Who or what is going to make the biggest difference to investors in the domestic stock market over the next few months? Will it be Sir Keir Starmer, Taylor Swift or Harry Kane?

As I’m part of a firm with a proud Scottish heritage, I would say don’t ignore the Tartan Army when it comes to the UEFA European Football Championship, but I can’t say with any certainty whether it or the Three Lions will make it to July.

And as a long-term investor I wouldn’t base any decision on what I think may or may not happen over the summer, but it does throw up a couple of opportunities to access the market which to me and my co-manager Ambrose Faulks still looks undervalued.

The main news from a UK perspective has been the decision by the Government to call a July election, which we view as broadly supportive of the market as it provides an early clearing event for a ‘known unknown’.

The significant Labour majority has in our view reduced the risk of more extreme elements of the party dragging its policies off to the left.

We got more details of actual policies from the main parties when they published their manifestos which didn’t produce any fireworks such as former Prime Minister Theresa May’s dementia tax.

Since the announcement, the FTSE 250 has outperformed the FTSE 100, suggesting the market has a similar view on the election to ours1.

Currency movements

Given the lack of sector-specific taxes or policies, we are of the view that the biggest market impact is likely to come through FX.

Here we can see scope for sterling to move higher if the Labour post-election ‘pro-growth plan’ for the UK is viewed as credible, thus reducing the elevated risk premia that the UK market has suffered from over the past eight years.

This has the potential to be magnified if the Bank of England holds off on cutting rates while the ECB and others move ahead.

On the economic growth side, there should also be the potential for a bounce in consumer confidence as the current Government has become synonymous with the ‘Broken Britain’ narrative.

This is where Harry Kane and the England team, Scotland’s John McGinn and the Tartan Army, and Taylor Swift could all contribute to consumer confidence.

One of our holdings, Mitchells and Butlers, recently reported strong results driven by an increase in operating margins to 11.7%. We expect further strong momentum through the summer as the number of licensed outlets across the hospitality sector continues to decline, meaning those left will only get stronger. This trend should long outlive this summer’s Euros.

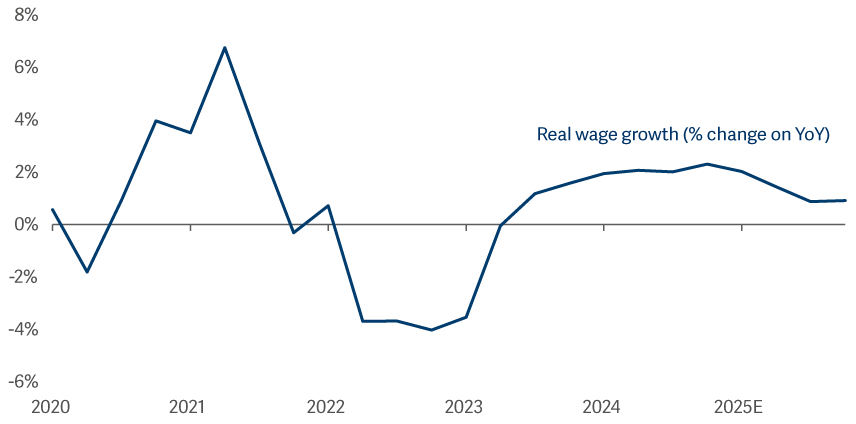

We expect the UK economy to accelerate, driven by a pickup in consumer spending – rising real wages2 and falling tax rates3 are all aiding cashflow, while pent-up savings remain high4.

Real wages have turned positive

Confidence boosts

In our opinion, the consumer is well placed to spend more as confidence improves. Some of that is already being driven by the economic phenomena known as “Swiftonomics” – the economic influence of Taylor Swift.

She kicked off her tour of England, Scotland and Wales on the 7th of June in Edinburgh and concludes at Wembley on the 20th of August.

It was estimated that Swift’s tour generated $5 billion in consumer spending across the US5 – could she produce a similar effect here?

Now imagine if Harry Kane lifts the European Championship trophy – the impact on GDP could be bigger than Taylor Swift’s!

2Lazarus Economics & Strategy/ONS as at 31 March 2024.

3Lazarus Economics as at 31 March 2024.

4Bloomberg as at 31 December 2023.

5https://ifamagazine.com/are-leading-brands-about-to-have-their-taylor-swift-moment-artemis-ramachandran-examines-swiftonomics-in-context-of-chinese-tourists/