Emerging markets: three catalysts for change

After a disappointing start to the year for emerging markets, valuation multiples have fallen to multi-decade lows relative to their counterparts in the US. Raheel Altaf asks whether that discount can last – and examines the factors that might trigger change.

- After a disappointing run, emerging markets now trade at multi-decade lows relative to US equities.

- Stimulus measures in China and falling interest rates elsewhere should offer powerful support to demand from here.

- The strategic case for investing in emerging markets remains intact – and weakness seen in the first half of this year may offer an attractive entry point.

You won’t be surprised to learn that we are strong believers in emerging markets. We think they offer invaluable diversification to most investors, whose portfolios are (increasingly) dominated by a handful of large companies in developed markets, particularly the US. And the long-term outlook for many emerging economies – in terms of their growth, demographics and consumer demand – is compelling.

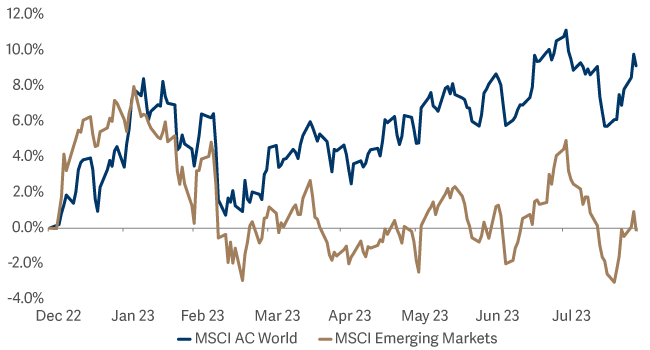

So when emerging-market equities began 2023 by moving sharply higher, boosted by optimism about China’s post-pandemic reopening, we thought their gains were richly deserved. Sadly, January’s rally proved to be short-lived: despite their early promise, emerging-market equities have again trailed their developed market counterparts this year.

After a strong start to the year, returns from emerging markets equities have faded. But where next?

Explanations are easy to find. Investors’ attention has been focused on US inflation readings, on monetary policy – and their impact on the US dollar and the wider global economy. Meanwhile, geopolitical worries, whether over Russia or China, have been at the forefront of investors’ minds, contributing to a more risk-averse environment in which emerging-market equities have (on aggregate) underperformed.

Is this underperformance warranted?

And, if not, what catalysts might encourage that to change? The long-term case emerging markets is familiar. But why should you look at them now?

1: China has announced substantial policy support

One key reason emerging markets have delivered such lacklustre returns this year has been disappointing news from China. While the Chinese economy grew at a healthy pace in Q1 (up 2.2% on the previous quarter), growth slowed to just 0.8% (quarter-on-quarter) in Q2. That growth fell so far short of expectations was attributed to weak demand at home and the struggles of the real-estate sector. This weakness appeared to be confirmed in July, when China reported worse-than-expected data for both imports and exports.

The important point, however, is this: policymakers in Beijing aren’t standing idly by while their economy stalls. News that the consumer prices had tipped into deflation was enough to convince them to take more direct action to shore up demand. An unexpected cut to one-year lending rates in mid-August could prove to be the start of more substantive policy action. And while hopes that China will deploy a stimulus ‘bazooka’ may be somewhat optimistic, we do expect continued and measured accommodation through the rest of this year. These measures are likely to bring further confidence to the consumer recovery story – and could prove decisive in changing sentiment towards emerging-market equities.

2: Emerging markets are beginning to enjoy a more supportive interest-rate environment (as well as stronger economic growth)

Look beyond China, meanwhile, and the path being taken by monetary policy in other emerging markets is increasingly diverging from the developed world. Chile led the way by cutting rates in July. Brazil – where headline inflation has fallen from 12% to a touch over 3%1 – followed suit at the start of August, cutting the Selic rate and indicating that more cuts would follow. In terms of GDP growth, meanwhile, emerging market economies are, on aggregate, forecast to grow by 4.0% this year and by 4.1% in 2024. While this is below their long-term average, it is well ahead of developed economies, where growth is expected to come in at just 1.5% this year and 1.4% next year2.

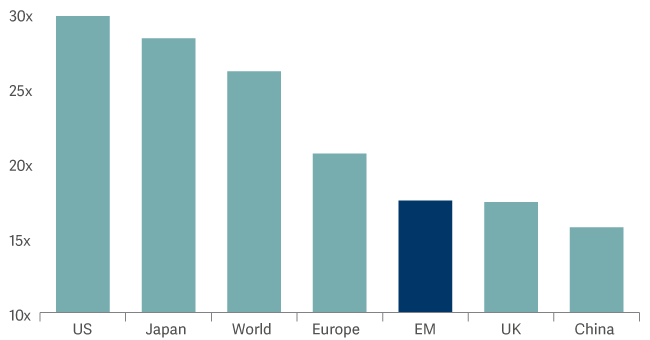

3: Valuations: emerging markets are now trading at multi-decade lows relative to US equities

Another potential catalyst for change is the striking disparity in relative valuations. Look at cyclically adjusted valuation multiples and emerging-market equities are now trading at multi-decade lows relative to their US peers. The cyclically adjusted Shiller p/e ratio (which takes a longer view of corporate earnings to smooth out temporary fluctuations in profits caused by business cycles, isn’t infallible) but it has been a powerful predictor of long-term equity returns. And as macro worries ease, we suspect investors will begin to refocus on relative valuations.

When they do, we believe they’ll find the valuation story in emerging markets compelling. We use a systematic process to screen the global equity market for companies whose prospects for growth are currently undervalued. For some time, that process has been giving us a clear signal: ‘value’ stocks in emerging markets offer some of the best value of any equity markets in the world. This, in our view, provides useful downside protection.

The cyclically-adjusted Shiller p/e ratio suggests emerging markets are attractively valued compared to their global peers

The longer-term case for emerging markets remains compelling

Of course, the case for allocating to emerging markets isn’t simply about protecting against the short-term downside – it’s about capturing the potential long-term gains. Here too, the conditions appear supportive. To recap:

- favourable demographics should support longer-term economic growth, driven by demand from local (rather than Western) consumers.

- growing middle classes and greater urbanisation are stimulating demand and helping to create local companies in emerging markets who will be the global leaders of tomorrow.

- the steps that economies – particularly in Asia – have taken to insulate themselves from demand shocks from the West mean they are becoming increasingly self-sufficient.

- a number of developing economies boast abundant natural resources, demand for which will increase as the energy transition accelerates.

When will the potential of emerging markets be reflected in improved share-price performance?

Putting the longer-term arguments for allocating to emerging markets to one side, looser monetary policy in emerging markets and better sentiment towards China may provide the catalyst for improvement in relative returns.

Market timing is, of course, an inexact science. But we would remind investors that the point of maximum financial opportunity often comes at the point where pessimism is at its most extreme. It is possible that we now are at – or approaching – that point. It is always darkest just before the dawn.