Explaining our hang-up with telco bonds

On the face of it, the telco sector should carry a degree of protection – even if there is a downturn, people will continue to pay their phone bills. But high levels of debt and low barriers to entry mean the sector looks vulnerable – as do the funds exposed to it, writes Jack Holmes.

Last month, many of the UK’s biggest high-yield bond managers got stung when the French telco business Altice proposed haircuts on the value of its debt. In the space of three days, the bond fell 45%1.

The irony is that this crisis was well telegraphed. Telco is a big part of the high-yield index but we have hated the sector for a long, long time. If the fund you invest in or recommend to clients maps the index – as a lot, sadly, do – then this crisis will have hurt. Some of the bigger houses hold over €200m2 of these troubled Altice bonds.

On the face of it, the telco sector should carry a decent degree of protection. After all, if there is a serious economic downturn tomorrow, people will still pay their phone bills. It is one of the last things they want to lose.

Why so negative, then? There are two main reasons – leverage and leeway. Let me explain.

In the era of quantitative easing, telcos gorged on cheap debt, becoming highly leveraged, spending on capex projects costing billions. They have bought 5G spectrum licences – arguably overpaying massively – and installed expensive new 5G infrastructure. All this just to stand still.

This investment has added little incremental profitability. Has 5G yet transformed your experience as a phone user to the point that you’d be prepared to accept a big hike in your bill to access it? Thought not. The reality is that this is an entirely commoditised market. Telcos have little leeway to raise prices sharply. We can switch contracts far too easily.

Now interest rates have risen, and the bill for this past profligacy has landed.

Lessons for investors

There are a number of lessons investors might take from the Altice story – not all of them right.

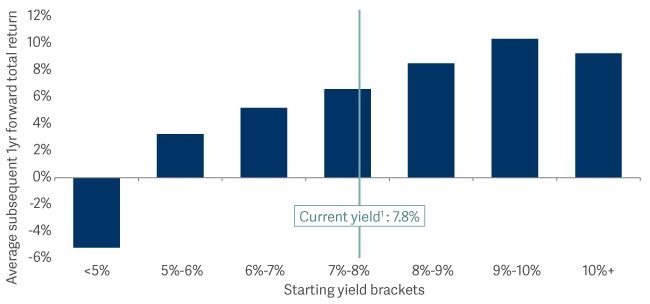

The first is that high yield isn’t worth the risk. This is just not true. Actually, with a yield of something in the region of 7.8%, I think it can bring a lot of value to client portfolios – and history suggests this will endure for at least a year (see the bar chart below).

Yields in mid-high single digits generally result in similar 1yr forward total returns

Those attractive returns obviously come with risk. What you need to know is how well that risk is being managed. High-yield bond investors have to look beyond just whether a business is cyclical or non-cyclical. We have to look at debt levels. And we have to look at profits and cashflow – something more normally associated with our colleagues managing equities.

So how do you know if your bond manager is doing that? How can you assess whether an active high-yield bond fund is actually active? One clue is how many positions it holds. Many will hold over 400. When that happens, there is realistically little credit selection happening. The other clue is when the fund has its biggest exposure to the largest names in the index. By default – or, rather, self-evidently – the biggest are the most indebted. And, of course, the most indebted are the most at risk of default.

Of course, you also want diversification. Even the best-researched business can be subject to external shocks or fraud. Hubris in thinking you can completely avoid problems is dangerous. But if you do your job as an active manager, you should be able to avoid many of the worst.

So, what is optimum? For us, somewhere between 90 and 100 companies feels right. That’s enough to demonstrate conviction – each holding matters, so you have to give it the research and attention needed in if you are to generate index-beating returns while still delivering sensible protection to investors.

Hang up?

The Altice crisis should be an alarm call for high-yield bond investors and their advisers in a world of higher-for-longer interest rates. You need your chosen high-yield manager to be truly active. If they are not, it might be time to ring the changes.